Kenneth Glad

Kenneth Glad

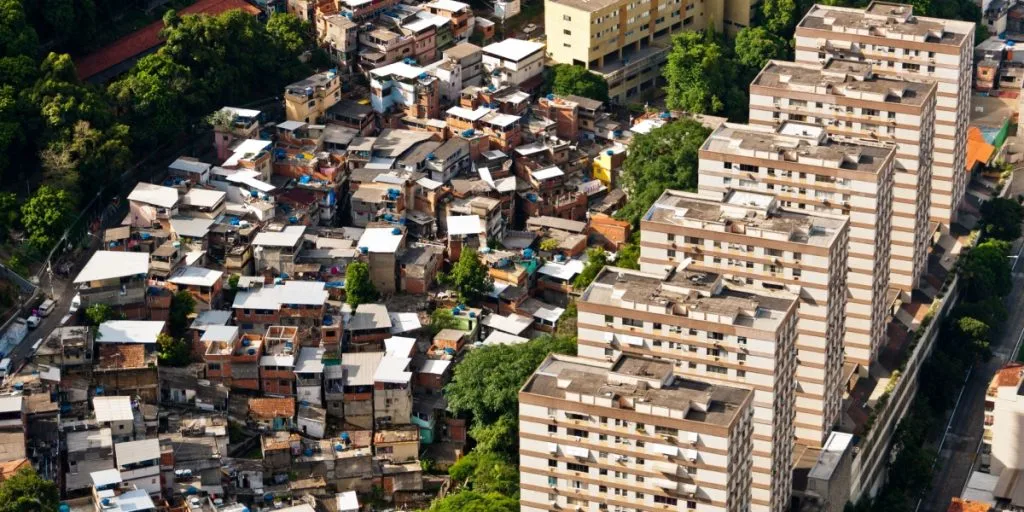

A growing number of wealthy investors are questioning whether the economic ideas that enriched them are sustainable. The concern is not just fairness, but whether an economy that concentrates wealth too narrowly can remain stable over time.

Nick Hanauer has spent decades on the winning side of American capitalism, backing companies and building wealth in the process. That is precisely why his public critique lands so sharply.

In two TED Talks, in 2014 and 2019, the Seattle venture capitalist aimed his argument at the people least likely to hear it: The ultra-rich, corporate leaders and the economists who justify policies that keep more money flowing upward.

What makes Hanauer’s case unusual is its framing. This is not a plea for charity. It is a warning that an economy built to enrich a small slice of society can end up endangering the system that made that enrichment possible.

An unlikely messenger

Hanauer introduces himself as “one of those .01 percenters that you hear about,” and speaks as an “unapologetic capitalist.”

In the talks, he lists a career that includes founding, co-founding or funding dozens of companies, plus being “the first non-family investor in Amazon.com.”

He also punctures the mythology that often surrounds extreme wealth. “Truly, my success is the consequence of spectacular luck, of birth, of circumstance, and of timing,” he says, arguing that vast fortunes are not reliable proof of being the smartest or hardest working person in the room.

That tension, beneficiary and critic, is the core of his appeal. He speaks as someone who understands how elites talk to each other, and how they talk to everyone else.

The economic story machine

In the 2019 talk, Hanauer argues that policy is steered by stories dressed up as objective science. He portrays modern “neoliberal” economics as a narrative that flatters the powerful: Taxes on the rich allegedly slow growth, regulation is inherently inefficient, and higher wages supposedly destroy jobs.

He calls those assumptions not merely mistaken but socially corrosive, because they imply that selfishness is the engine of prosperity. If that worldview is accepted, then widening inequality can be framed as efficient rather than dangerous.

Hanauer’s counterclaim is that an economy does not run on the genius of a few winners. “It turns out it isn’t capital that creates economic growth, it’s people,” he says, adding that reciprocity and cooperation matter far more than the caricature of humans as relentlessly self-maximizing.

This is where he shifts from ideology to mechanics. Prosperity, he argues, is what happens when more people can participate fully, as workers, customers and problem-solvers.

Wages as a growth lever

Hanauer’s wage argument is less about compassion than about throughput. If pay stays low and insecure, households trim spending. Businesses then face weaker demand, and the supposed dynamism of the market starts to look brittle.

He delivers the point with a line that became a signature: “I earn a thousand times the median wage, but I do not buy a thousand times as much stuff, do I?” The wealthy, he argues, hit a ceiling on consumption. The broad middle does not, because millions of everyday purchases are what keep local economies moving.

In other words, the question is not whether the richest people can afford more. It is whether the rest of the economy can afford to be customers.

That is why he tries to reframe “job creation.” In his telling, hiring is a response to demand, not a gift from investors. The middle class is not the after-effect of growth. It is a major ingredient of it.

What Seattle was meant to prove

To ground the argument, Hanauer points to Seattle’s minimum-wage fight, describing it as a real-world test of a popular warning: Raise the “price” of labor, and employment will fall.

Seattle, he notes, approved a plan in 2014 to raise the minimum wage to $15 an hour, a move that triggered dire predictions about restaurants closing and low-wage workers being priced out of jobs.

In his TED framing, those predictions did not materialize in the sweeping way opponents promised. He argues the reason is intuitive: Higher pay increases households’ spending power, and that spending power loops back into the local economy as revenue for businesses.

He also makes a rhetorical move that is easy to miss: He challenges the idea that labor markets behave differently from executive labor markets. CEO pay, he says, exploded over decades, and companies did not respond by eliminating CEO jobs. In his view, that undercuts the simplistic claim that higher labor costs automatically mean fewer workers.

Economists still argue over how minimum-wage increases play out across different regions and industries. Hanauer’s point is narrower: The knee-jerk certainty of catastrophe has become a political weapon, not a careful forecast.

A compressed Ford lesson

Hanauer reaches for Henry Ford as a shorthand for a larger idea: the wage bill can be part of a growth strategy, not just a cost to squeeze.

When Ford raised factory pay, Hanauer argues, it did more than reduce turnover and stabilize production. It also expanded the pool of potential customers, turning workers into consumers who could afford the product ecosystem they supported.

This is not presented as nostalgia for a lost era. It is a reminder that mass-market capitalism depends on mass-market purchasing power. When workers are permanently priced out of the very economy they staff, the system becomes lopsided.

Even in modern industries that are less like assembly lines, the same basic constraint applies. If demand is concentrated among a small group, the economy’s growth potential becomes constrained by how much that group can plausibly buy.

The “pitchforks” warning

Hanauer’s summarising in his 2014 talk arrives as a forecast, not a threat. “I see pitchforks,” he says, predicting anger from people who feel locked out while a small elite “live beyond the dreams of avarice.”

He cites wealth-share figures to argue that inequality in the United States has risen sharply since 1980, and he paints a historical analogy: When societies let wealth and power pool at the top, the result is often repression, upheaval, or both.

“You show me a highly unequal society and I will show you a police state or an uprising,” he tells the audience, framing the risk as structural. In his view, free and open societies do not remain stable indefinitely under extreme concentration.

The line travels because it is blunt. But the surrounding argument is practical: instability is bad for business, bad for investment and bad for the wealthy who assume their security is permanent.

Choosing a different capitalism

Hanauer does not argue for ending capitalism. He argues for managing it, on purpose.

He calls for abandoning trickle-down logic and replacing it with what he describes as “middle-out economics,” a view of the economy as a complex system that tends toward concentration unless actively counterbalanced.

That leads to a policy menu he portrays as pro-capitalist rather than anti-business: wages that support a decent standard of living, affordable health care, paid sick leave, investments in education and research, and progressive taxation to fund shared infrastructure.

He also offers a strategic answer to a familiar challenge. When asked why not simply give away more money personally, he says that individual generosity is dwarfed by changing the rules: “I have discovered a strategy that works literally 100,000 times better, which is to use my money to build narratives and to pass laws that require all the other rich people to pay taxes and pay their workers better.”

He closes with the same fork in the road that runs through both talks: Reform the system to keep it durable, or retreat into private comfort and denial.

“Alternatively, we could do nothing,” he says, and “wait for the pitchforks.”

Sources: TED Talks by Nick Hanauer (2014; 2019).